New Book Is On the Way. My last post, Public Markets Provide Context for Private Company Valuation, was actually the first in a series of posts that will eventually be turned into my next book, which will be a non-technical and informative book for business owners. The working title is Business Valuation for Business Owners, but that will likely change before it is completed. This will be the third book I’ve written in installments on one of my blogs. The first two were Buy-Sell Agreements for Closely Held and Family Business Owners and my latest book, Unlocking Private Company Wealth. I’m excited to have another book on the way. Please do share your thoughts by commenting on the blog or directly to me. Now, let’s continue with the expectational nature of business valuation.

Value is all about the future and not the past. With a minimum of math/algebra, let’s see what this means and get to the point. Most everyone is familiar with what I call the basic valuation equation, even though they may not use that term. Simply stated, it is this:

We will discuss that equation after a very short look at valuation theory so that we can have an understanding of where this simple equation comes from and what it means. But don’t let that theory word get to you. This discussion will be short and will, hopefully, make us think about business valuation in a different light.

We can define the value of a business in words as follows:

The value of a business, today, is the present value of all expected future benefits (i.e., cash flows) to be derived from that business from now until the indefinite future, all discounted to the present at a discount rate reflective of the risks associated with achieving those benefits or cash flows.

Business valuation is a present value concept that converts the expectation of future benefits into present (valuation date) value. The benefits of the business being valued are not the past benefits, although they will inform the analyst about the future. The benefits being valued are expected future benefits. This means that business valuation requires some form of forecast of the future

Revenue Ruling 59-60, published by the Internal Revenue Service in 1959, defines the standard of value known as fair market value used in all gift and estate tax valuations and many others. We will talk about fair market value after we understand the basics of business value. RR 59-60 states, in part:

Valuation of securities is, in essence, a prophesy as to the future and must be based on facts available at the required date of appraisal

Many analysts use a model known as the discounted cash flow model, or the DCF model, to estimate business value in the context of the definition above and to “prophesy” the future.

Discounted Cash Flow Method (DCF)

In theory, the DCF model requires a forecast of expected annual cash flows for every year after the valuation date into the indefinite future. Valuation is a perpetuity concept. The business is expected to continue to generate cash flows into perpetuity.

Algebraically and conceptually, the DCF model looks like this:

{kind=link}

In the equation CF1, CF2, and so on in the numerator are the forecasted (expected) future cash flows for period 1, period 2 and so on. The periods are almost always annual periods. CFn is symbolic of forecasting into the indefinite future. So the DCF model requires a forecast that goes on, literally, forever. That’s not very practical, but it is a start to a simpler approach.

r is the discount rate developed by the valuation analyst that reflects the risks associated with achieving the forecast. We will talk more about this r, or discount rate, but accept it symbolically for now.

The calculations suggested in the equation above provide for discounting of expected future cash flows to the present.

There are at least three problems with this formulation of the DCF model.

- The model is not reflective of how we think about valuation, except conceptually

- No one can realistically and reliably forecast into the indefinite future

- The formulation is quite cumbersome

There has to be a better way. So we jump the gun a bit to the Gordon Growth Model.

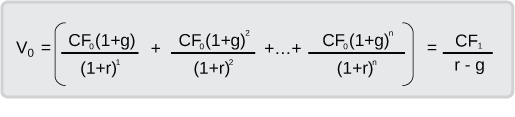

The Gordon Model

In a 1962 text, Professor Myron Gordon proved, and we’ll believe him, that the equation above could be simplified to the following equation:

The expected future cash flows are the net cash flows to the equity holders of a business. The V, or Value derived is the value of all of the equity of the business. The notation is for time period zero, or now, to distinguish today’s value from the expected cash flows for period 1. Now that we’ve said that, just ignore the technicality. We will see shortly why it is important to know that this equation values the equity of businesses.

The Gordon Model equation is really a forecast, under simplifying assumptions, into the indefinite future. This is very convenient and will help with employing discounted cash flow in valuations. This equation works under three simplifying assumptions:

- The expected cash flows must be reinvested in the business at the discount rate, r. Alternatively, they can be paid to shareholders as dividends.

- The growth rate, g, is a constant growth rate into the indefinite future, i.e., it is a long-term growth rate.

- The discount rate, r, must be the appropriate discount rate that is reflective of the risks associated with achieving the expected future cash flows.

With Professor Gordon’s breakthrough work, analysts were then able to develop what is called a two-stage DCF model.

Two-Stage DCF Model

In the two-stage model, the analyst forecasts cash flows for a finite period of years, quite often five years (or three years or ten years). Conceptually, the two-stage DCF model looks like this:

Look at the left side of the equation. It is labeled as the present value of interim cash flows. The basic idea of the two-stage DCF model is for the analyst to forecast for a finite period of years, or enough years until earnings and margins are projected to stabilize.

The near-term expectations for companies can differ from recovery from historical losses, to steady-state growth, to rapid growth, to cyclical growth, depending on the circumstances in existence when a company is being valued. Practically, analysts are better able to forecast specifically in the near term than in the longer term. So we forecast for an interim period whose length is determined by the valuation analyst.

Each of the interim cash flows is discounted to the present at the determined discount rate, r. The sum of these calculations is called the present value of interim cash flows.

Now look at the right side of the equation. It is labeled the present value of the terminal value. At the end of the finite forecast period, analysts can use Professor Gordon’s model, called the Gordon Model, to estimate the value of the terminal value, or all remaining expected cash flows beyond the forecast period. That terminal value is then discounted to the present (again, using r) and this is called the present value of the terminal value.

The conclusion of the two-stage DCF model is the sum of the present values of the interim cash flows plus the present value of the terminal value.

In typical DCF valuations, the terminal value will account for 60% or more of the total value being determined, particularly in three and five year forecasts. If a company is forecasted to have near-term losses and then recover to significant profitability over the forecast period, the terminal value estimation may account for 80% or more or the overall value.

We have now developed the conceptual two-stage DCF model that is employed by valuation analysts and sophisticated market participants in less than one thousand words. That’s as brief as I can make it. We will show how this model works in practice as we proceed.

Now, let’s remember the Gordon Model:

We will use this model to learn a great deal about the value of closely held and family businesses and develop what I call the basic valuation equation.

In the meantime, be well.

Chris

I am valuing a 50/50 interest in an LLC.

The operating member says he wants the cash flows based on the last 12 months earnings.

He wants to buy out the passive member who guarantees all the bank debt.

His CPA says it is customary to value on past 12 months as an estimate of future growth and at a minority marketable discount as well. This is supposed to be a friendly buyout so the younger guy prevents gifting of the older guy to people he does not want to have a voice in the business,

Is this rational still prevalent in practice or just a negotiating strategy. The business is logistic and the business is located near the L.A/Long Beach ports and is growing at the rate of 4% annually.

There is no buy/sell agreement in place.

Would you care to comment

Gil,

With shareholder buyouts where there is no buy-sell agreement place, there is no “customary.” The buyout, if it occurs, will be the result of, hopefully, friendly negotiations. I doubt that the money partner will accept a discounted value. Why should he? Of course, the operating guy would like to buy the company cheaply, but it likely won’t happen unless the money guy is under duress.

Why don’t they agree that the buyout would be at the valuation you provide at the financial control level. That level is described pretty well in my book, Buy-Sell Agreements for Closely Held and Family Business Owners, as well as a single appraiser process for a workable buy-sell agreement.

I think the CPA should read my book and reconsider what he things is “customary.” It sounds like the money guy is content with his distributions and would make gifts to his kids or someone. If he is willing to entertain a sale of his 50%, then the operating guy should be putting together an attractive offer that is supported by valuation and logic.

And regardless, I’d suggest that they put a buy-sell agreement in place pronto. Time has a way of passing and things like buyouts have a way of not happening. Both parties are at risk in this situation. The discussions over its terms would no doubt inform both sides each other’s thinking. Use my Buy-Sell Agreements Review Checklist, available on this blog in the Store as a complimentary download, for some thoughts about possible terms and an outline for the agreement.

Thanks for the question!

Chris

Chris – good start, but consider the audience – CEOs. Something simpler than earnings x multiple might be V = reward/risk. Best regards and I will be looking out for the new book. Brooke

Brooke,

Thanks for the note. When you get to it, value is all about expected cash flow (rewards), risk, and growth. I agree that owners need to focus on rewards and risks, but a thought or two about growth isn’t bad, as well.

I’ll pull the book together from a series of posts on this blog. It is motivating to try to keep a schedule now with a specific goal in mind.

Hope to see you soon,

Chris