The Tax Cuts and Jobs Act of 2017 was signed into law by President Trump on December 22, 2017. President Trump calls the bill the biggest tax cut in American history, and there were substantial reductions in both corporate and personal income tax rates.

The tax reduction act will impact C corporations as well as pass-through entities. This post focuses only on C corporations and looks at the marginal impact of the change. In the words of that famous economist, “all other things will be held equal” as we examine the potential impact of the new tax law on privately owned C corporations.

Corporate Taxes are Lowered

Upon Mr. Trump’s election in late 2016, the stock markets began to anticipate that he would follow through on his campaign promise to cut business taxes in order to make American corporations more competitive internationally.

As of early February 2018, the broader market indices are up well more than 20% since late 2016.

That is the result in the public markets. Will valuations of privately owned C corporations automatically rise 20%? At this point, with the passing of December 31, 2017, thousands of private companies across the nation must be valued for a variety of reasons. Business appraisers will have to begin to consider the impact of the tax act on the coming wave of appraisals.

Basic Valuation Equation

I’ve spoken about the “basic valuation equation” a number of times on this blog.

Value = Earnings x Multiple

All appraisers have to do is to determine the relevant Earnings and then, the relevant Multiple to arrive at Value. I’ve also said many times that if valuation were actually that easy, I and many others would not have enjoyed great careers in the appraisal profession. Other things are not always equal….

C Corporation Earnings

We know that the federal corporate marginal tax rate was lowered from 35% to 21%. Given the impact of state taxes on C corporation earnings, appraisers have historically used a blended federal/state tax rate of 38% to 40%. For our purposes here, assume that the old blended tax rate was 38%.

With the reduction in the federal rate, there will be an accompanying reduction in the blended tax rate. Assume that the new blended federal/state tax rate for C corporations is 25%.

What happens to expected earnings when we compare the new tax rate with the old rate? For a given dollar of pre-tax earnings, less taxes will be paid, so after-tax earnings will rise. We see this in the table below.

For a given dollar of Earnings Before Interest and Taxes, which can also be called debt-free pre-tax earnings, debt-free net income is $6.2 million under the old tax law and rises some 21% to $7.5 million under the new law. Looking at the basic valuation equation above, Earnings should be up under the new tax law so, other things being equal, value should rise.

After-Tax/Debt Valuation Multiples

Business appraisers develop discount rates and valuation multiples in virtually every valuation. We do so using one of several forms of what I call the Adjusted Capital Asset Pricing Model. I used this model when I first addressed the prospective impact of Mr. Trump’s planned corporate tax reduction on valuation multiples in May 2017.

In the table below, we develop discount rates for a generalized and hypothetical private company which is organized as a C corporation. We calculate discount rates under both the old tax law and the new tax law. The assumptions leading to the equity discount rate are not controversial, and the concluded equity discount rate is 14.9% under both laws.

The discount rate is geared to reflect risks associated with a reasonably attractive privately owned C corporation. The assumptions for the components of the discount rate are selected so as not to be controversial. Note that in leading to the equity discount rate above, nothing changes, at least directly as result of the tax act. To be clear, there is no direct impact from the tax reduction on any of the components (see Lines #1-#6 above) of the equity discount rate (Line #7) under either scenario.

We use the equity discount rate as one component of the build-up to reach the enterprise level discount rate, or weighted average cost of capital (WACC). The second component of WACC begins with the pre-tax cost of debt, which we have assume here to be 6.0% (Line #8 below). We calculate taxes based on the old and new tax laws.

The after-tax cost of debt under the old law is 3.72%, while the after-tax cost of debt under the new law is 4.50% (Line #10). In a way, this is counter-intuitive, but the tax shield is lower under the new law so the after-tax cost of debt rises. This means that there will be an upward bias on the after-tax WACCs of C corporations under the new law.

The assumed capital structure above is 75% equity and 25% debt (Lines #7 and #10), a reasonable and general assumption. There will be a modest upward bias on the WACC as result of higher after-tax interest expenses.

On Line #11, we see that the WACC under the old law is 12.11%, while the WACC rises to 12.30% under the new law. This is not a lot of change (1.6%). We assume a long-term growth rate of 3%, another reasonable assumption (Line #12). This growth rate is subtracted from the WACCs to achieve the debt-free capitalization rates of 9.11% (old) and 9.30% (new) on Line #13. Again, this change is small (up 2.1%).

The debt-free net multiples are derived on Line #14 as 10.98x (old) and 10.75x (new). As with the change in cap rates immediately above, the change in debt-free multiples is also small (down 2.1%).

Summarizing the implications of the new tax act on C corporation private companies to this point, we see that there should be little change in after-tax multiples and a significant change in after-tax earnings.

Before-Tax/Debt Valuation Multiples

We now look at the pro forma impact on enterprise multiples of EBIT and EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization) using a continuation of the analysis found in Lines #7-#19 above. We will focus on EBITDA for the most part.

Keep in mind that since both EBIT and EBITDA are before taxes, there will be no change to these measures of cash flow based solely on the tax law change.

We can convert after-tax capitalization rates into before-tax cap rates as shown on Lines #13-17 by dividing them by one minus the (old and new) tax rates. At this level, we see a significant difference in cap rates. The EBIT cap rate under the old law is 14.69% while the EBIT cap rate under the new law is 12.40% (Line #16), reflecting a reduction of 15.6%.

The lower EBIT cap rate under the new tax law suggests that the implied EBIT multiple will be significantly higher than under the old regime. The old EBIT multiple is 6.81x and the new EBIT multiple is 8.06x, or 18.4% higher (Line #17).

An EBITDA depreciation factor of 1.25x reflects the average relationship between EBIT and EBITDA for a substantial portion of the public company marketplace.

The EBITDA Depreciation Factor measures the relationship between EBIT and EBITDA and is one measure of capital intensity. The higher the factor, the greater is EBITDA in relationship to EBIT. The factor can be calculated: Factor = EBITDA/EBIT.

We use this general factor of 1.25x on Line #18 above to convert EBIT multiples to EBITDA multiples. The implied EBITDA multiple under the old tax law was 5.45x, while the multiple under the new tax law is 6.45x, or a turn higher (Line #19) under the assumptions above and assuming that nothing else in the world changes other than the tax rate.

Impact on Value

We have now looked at debt-free after-tax cap rates and multiples under both the old tax law and the new law. And we have looked at pro forma changes in before-tax multiples of EBIT and EBITDA. What happens to value? The following table looks first at the capitalization of debt-free net income and then of EBITDA. If our theory makes sense, then the analysis results should also make sense.

We see on Lines #20 and #25 that EBIT is unaffected by the change in corporate tax rates. We assume above that EBIT is $10.0 million initially, and it remains the same before and after the corporate tax reduction.

On Lines #21 and #22, we see that the tax reduction results in a substantial increase in after-tax income. As noted above, debt-free net income rises from $6.2 million to $7.5 million on a pro forma basis (again, other things being equal).

With the only modest reduction in the debt-free net income multiple (Line #23), the rising income swamps the negative impact of multiple reduction, and value rises from $68.1 million to $80.6 million, or 18.4%.

On an after-tax basis, the story is that earnings rise substantially, driving a large net increase in pro forma value.

Lines #25-#27 calculate EBITDA based on the assumed EBIT and the assumed EBITDA depreciation factor of 1.25x. EBITDA under these assumptions is $12.5 million. The EBITDA multiple rises from 5.45x to 6.45x, or 18.4%.

Since there is no change in EBITDA under the new law, the implied EBITDA multiple increase of 18.4% yields a new, pro forma value of $80.6 million, or the same as calculated above with after-tax multiples. That makes sense because we are valuing the same company.

Initial Observations

We can make a number of observations from the above analysis of the impact of the new tax law on cash flow, valuation multiples, and value. All summaries are based on the economist’s assumption that all other things – other than the tax law change – remain equal. Summarizing for after-tax valuations:

- With a reduction in the federal/state tax rate from 38% to about 25%, there will be a substantial increase in after-tax cash flow.

- The tax law change impacts the standard estimation of WACC only modestly through the increased after-tax cost of debt and lower tax shield from the lower tax rates.

- From an appraiser’s viewpoint, there is little impact on the traditional building-up of after-tax discount rates and WACCs (or at least, the increase is very modest).

- From an appraiser’s viewpoint, there will be a need to focus sharply on the prospective impact of lower taxes as well as other relevant factors, which, in the real world, are not held equal.

- Other things being equal, value should rise for privately owned C corporations as a result of the lowering of corporate tax rates. How much values will rise will depend on actual expected taxes as well as the other factors that will impact expected future cash flows for private companies being valued.

The reduction in corporate tax rates does not impact broad pre-tax measures of cash flow like EBIT and EBITDA.

- Other things being equal, EBITDA multiples will rise to reflect the higher values resulting from higher after-tax cash flows.

- Appraisers must be careful, however, in developing EBITDA multiples. The use of multiples from historical transactions involving “comparable” companies may be invalid for a few years until the majority of future-recent transactions are recorded under the new tax law with lower corporate rates.

- More appraisers are likely to begin to formulate EBITDA multiples using methods similar to those used above.

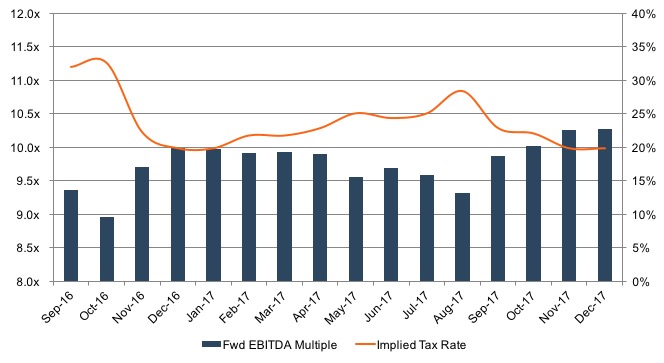

The following figure is from a presentation on Mercer Capital’s website. The figure examines smaller (non-financial) public companies over the period from late 2016 to the present.

The analysis above is in the Mercer Capital paper linked above. The analysis is another of those “other things being equal” things. Travis Harms went back to September 2016 before the election.

The analysis above is in the Mercer Capital paper linked above. The analysis is another of those “other things being equal” things. Travis Harms went back to September 2016 before the election.

{kind=link}

- The analysis looks at the S&P 1000, or non-financial public companies with about $500 million to $5 billion in market capitalization.

- At each month-end, the stock prices for each company and their forward estimates of EBITDA were downloaded.

- Simplistically, the model solved for the implied corporate tax rate that matched the then-current stock prices for each company in light of its forward EBITDA projections.

The implied tax rate started in the 30%-plus range, and fell quickly to the 20% range on optimism of a quick passage of the tax bill. As the year passed and the new tax bill did not, the implied tax rate rose back toward 30% as the year progressed. Later in the year, as the expectations for a successful passage of the bill increased, the implied tax rate fell to the range of 20%. The markets did indeed anticipate the passing of the new tax act and lower corporate taxes.

The result is that, as shown above, the broader markets are up more than 20% since late 2016. Forward EBITDA multiples, as calculated in the analysis above, have increased about a turn (or about 10%) to 10.3x at the end of 2017.

The real world examples are not as neat as my pro forma analysis above. However, in the real world, other things are never equal. The markets take into account many factors and recognize these in their collective valuations of corporate America. What’s different in the real world? Many things, including:

- The shareholders may not receive all of the benefit of lower taxes.

- Many corporations have announced $1,000 and $2,000 bonuses to be paid to all of their employees, and more companies are likely to do so. Corporate managers who are compensated based on earnings may also benefit somewhat.

- Some corporations have announced increases in corporate giving to charitable causes that will absorb some of the benefit.

- Corporations have announced new capital expenditures that will absorb some of the benefit of the tax savings. The shareholders certainly hope to benefit in the future, but the markets will take their time in evaluating these plans.

- Some corporations with market power may demand that their suppliers “give up” a portion of the benefit of their expected lower taxes in lower prices. Some clients have already received calls on this issue from their dominant customers.

Conclusion

The bottom line is that there are no simple answers to the question of post-tax reform valuation of privately owned C corporations. The focus of appraisers, however, will likely be more on the Earnings portion of the basic valuation equation, since the reform has little impact on the after-tax multiples.

Appraisers will, I believe, begin to seek new ways of developing pre-tax multiples. Reliance upon market transactions will be questionable for some time to come, since all historical transactions (i.e., prior to year-end 2017) occurred under a different tax regime.

Business owners who rely on so-called “rules of thumb” to estimate the value of their businesses had best seek professional advice. The valuation world has changed, indeed.

Business owners who have fixed price buy-sell agreements or formula-pricing buy-sell agreements should be rushing to have them updated to substitute appraisal processes. It should be clear from this post that there could be significant surprises in store for fixed-prices and formulas to determine pricing for buy-sell agreements. We will focus on this issue next.

I conclude this post with the note that this analysis relates only to privately owned C corporations. There are many other ramifications of the new tax law that we and others will be examining in the coming months.

Be well,

Chris

Reminder

Valuation is important for business owners for many reasons. One of these reasons is for the operation of buy-sell agreements. If you are thinking about your buy-sell agreement (and you should be), then take a look at Buy-Sell Agreements for Baby Boomer Business Owners, my Kindle book on the topic.

I’ve priced it at $2.99 so you won’t have to think about the expense. So click on the image of the book. You will be taken to Amazon. Then buy the book. Don’t be mislead by the price. It is a full-length book. If you like it, as most readers have, please take a few minutes and review the book on Amazon!

Additionally, my two most recent books are available in an Ownership Transition Bundle. The bundle, priced at $35 plus s/h, has been attractive to many business owners, appraisers, and attorneys.

Very interesting article. I just would add that higher cash flows could results in more investments or higher wages, and consequently higher inflation.

High inflation would raise the risk-free rate and the equity cost.

So, WACC would increase due to higher equity cost and lower debt benefits.

Many things can and will happen as result of the new tax law. The markets will absorb all information over time and respond as they deem appropriate. This analysis is “at the margin” and assumes the result of nothing else changed other than the tax rates. That gives us direction of change and order of magnitude. The article then notes a number of factors that can modify the indicated results.

Thanks for your comment!