In the last post, we defined buy-sell agreements (at least in terms of a layman), noted key business issues that must be addressed, confirmed that buy-sell agreements are common to all corporate forms and industries, and profiled the types of companies we are addressing. Now it is time for a quick look at the three main categories of buy-sell agreements.

The three categories are cross-purchase agreements, entity purchase agreements, and hybrid agreements. They are defined by the relationship between a corporation (or other business entity) and its owners who are subject to the buy-sell agreements.

Cross-Purchase Buy-Sell Agreements

Cross-purchase agreements are agreements between and among the shareholders of a corporation calling for the purchase by the other shareholder(s) of the shares subject to the buy-sell agreement. With cross-purchase agreements, each owner individually agrees to purchase the interest of an owner if one of the conditions that triggers the agreement occurs. Triggering events generally include the death, disability or retirement of a business owner or otherwise sale of a shareholder’s interest. The cross purchase agreement will outline the terms on which purchases/sales are to be made following trigger events. They will either provide for an agreed upon price (fixed price agreement), a formula, or a process to determine value for transaction pricing.

Normally, cross-purchase agreements call for remaining owners to acquire a selling/departing owner’s interest pro rata to their ownership. For example, assume there are five equal owners of a business, so each owner has a 20% interest. If one owner dies, the remaining four owners (holding 80%) would acquire the selling owner’s interest based on 20%/80%, or 25% each, for the interest. So each remaining owner would acquire 5% (i.e., 25% share times the 20% interest being acquired), and each remaining owner would then own 25% of the business.

As part of a cross-purchase agreement, the departing owner, or his estate if he dies, is also obligated to sell her interest in the company. With a cross-purchase plan, the company is not a party to the agreement.

Consider the following characteristics of cross-purchase agreements:

- They are often funded by life insurance owned by shareholder(s) on the lives of other shareholders. They become problematic if one or more owners is uninsurable or insurable at high costs because of medical conditions.

- Cross-purchase agreements can quickly become unworkable as the number of shareholders increases and as market value grows.

- Cross-purchase agreements are also used in many businesses that are owned by one family. They do so to avoid the potential tax problems inherent in the family attribution rules of the Internal Revenue Service.

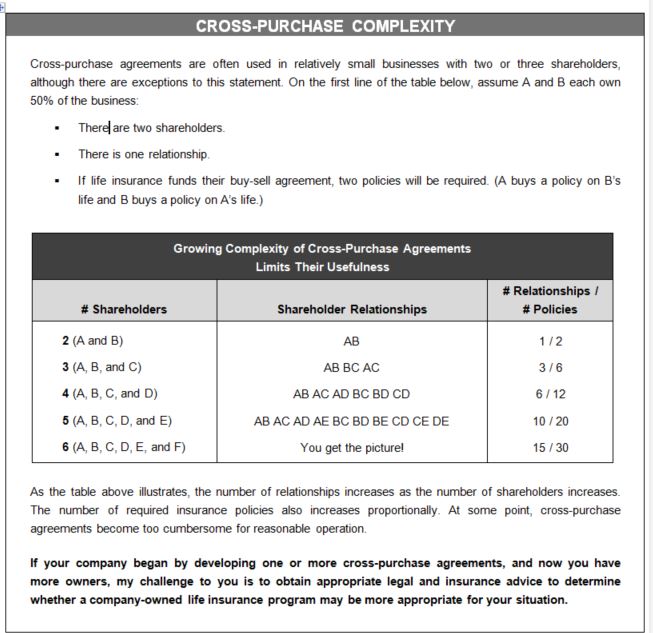

Cross-purchase agreements are fairly straightforward if there are two or three owners; however, they increase in complexity as the number of owners increases. For example, if a business has two owners, each owner would purchase a life insurance policy on the life of the other owner. At the death of one owner, the remaining owner would receive proceeds of his life insurance policy to be used to purchase the deceased owner’s interest. However, if the number of owners increases, the complexity of the arrangements increases as well, as seen in the following figure.

{kind=link}

Sometimes, life insurance specialists will suggest having a trust or a partnership acquire the policies on the lives of each owner, with each owner having his or her pro rata ownership in the trust the same as ownership in the business entity. I am not a life insurance specialist, and offer no advice in this regard.

We will not focus on cross-purchase agreements; rather, we focus on businesses with substantial value that are privately owned and have multiple owners. By the time most businesses achieve substantial value, they tend to use entity purchase agreements (or hybrid agreements).

Entity-Purchase Agreements

Entity-purchase agreements call for the corporation to purchase the shares upon the occurrence of trigger events. The entity (corporation) is then responsible for defining or providing the funding mechanism. Funding may be provided through the purchase of life insurance, financing by a third party or the selling shareholders, cash on hand, or a combination. We will discuss the various features of entity-purchase agreements as we progress.

Hybrid Agreements

Hybrid agreements generally call for the entity to have the right to purchase shares upon the occurrence of trigger events. They also provide the potential opportunity for remaining shareholders to acquire shares. For this reason, hybrid agreements are sometimes referred to as “wait-and-see” agreements. If a trigger event occurs, the corporation has discretion to either purchase the shares or to facilitate the purchase by the remaining owners. Everyone gets to “wait-and-see” whether it is more advantageous for the corporation or the other owners to purchase. However, control over the process should remain with the corporation in order to facilitate orderly transactions.

- In the event the corporation initially declines to purchase, it may have the right to offer the shares to the other shareholders pro rata or to selected shareholders.

- Hybrid agreements can be used to create non-pro rata changes in relative ownership if that result is desired for business reasons. Funding may be through a combination of self-financing by the corporation, notes from selling shareholders, and life insurance.

- Hybrid agreements often give the corporation a “last look” if shares are first refused and other shareholders do not purchase the stock. For the hybrid agreement to be effective, the corporation’s “last look” must be binding as to the purchase of the shares.

For larger corporations, most buy-sell agreements are entity-purchase agreements, or they are hybrid in nature if the corporation has the right to allow individual shareholders to stand in its place. For substantial corporations with more than a few shareholders, the preponderance of buy-sell agreements are entity-purchase agreements, some of which may allow the redirection of purchases to some or all shareholders under specified circumstances. Nevertheless, the corporation almost always has the last look and requirement to purchase. This is necessary to assure that a transaction is completed following a trigger event.

Next time, we will pick up with common trigger events for buy-sell agreements.

Until then, be well,

Chris

Reminder

My two most recent books are available in an Ownership Transition Bundle. The bundle, priced at $35 plus s/h, has been attractive for many business owners, appraisers and attorneys.

Please note: I reserve the right to delete comments that are offensive or off-topic.